House sales and homemovers play a significant part in boosting the furnishing industry. We take a look at how the housing market is changing through the new TwentyCi Property & Homemover Q1 2025 Report.

According to the latest research, the TwentyCi Property & Homemover Q1 2025 Report found that there were 451k new properties listed for sale during the period – the highest in the last seven years – driven by strong growth in properties priced between £350k to £1m.

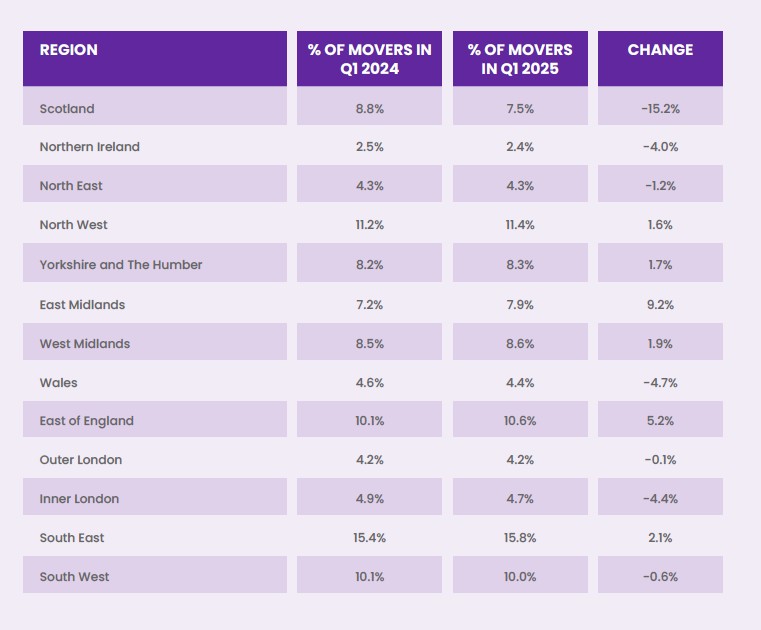

Demand for properties in 2025 is 9.3% higher than Q1 2024, with 326k sales agreed. Growth is observed across all UK regions, except Northern Ireland. Meanwhile, the supply of new instructions is up by 3.7% compared to Q1 2024. “We are now consistently averaging c425k per quarter which can be considered closer to the volume seen in a “normal” market,” the report states.

The East Midlands recorded the highest percentage of sales agreed at 14.2%, followed by the North West at 13.7%, with Wales and the East of England sharing third spot at 12.4%. In terms of major cities, Manchester led significantly with a 16.4% increase in sales agreed, followed by Newcastle upon Tyne at 12.5%. Scotland experienced more modest increases with Glasgow at 2.1% and Edinburgh at 1.9%.

Furthermore, the average time to get a sale agreed on a property has increased to 84 days in 2025, while the average time to exchange in the UK increased to 4.3 months. Exchanges are up by over 24%, with a significant number of these transactions will have been driven by the change to the stamp duty threshold that came into effect on the 1st of April. Detached houses are particularly in demand, with a 12.8% increase in the demand-to supply ratio compared to the previous year.

However, fall through volumes are also increasing, up by over 20%, which could be a direct consequence of the Stamp Duty change, with many sellers “abandoning” a transaction if the deadline for completion could not be achieved.

Shifting the focus to housing prices, the average asking price of residential properties for sale across the UK has remained static at £434k. There are regional variations where the North-East saw the largest increase in instruction prices, while Inner London experienced a decline.

As for the renting market, the continued duress of the sector is well documented through a combination of stock shortages, increased rental costs, and landlords exiting the market. New instructions are flat at +0.7% with let’s agreed up 6.7% and properties let marginally down by 0.5%. Based on the rental stock available, the average asking price is now £1,767 per month.

While Outer London led with the highest increase in lets agreed at 16.1% in Q1 2025 compared to Q1 2024, Inner London saw a more moderate rise of just 3.2%. The north of the country performed well, with the North East seeing an increase of 13.6% and Scotland experiencing a growth of 11.3%. Similar to the sales market, Northern Ireland was the only region to report a decline, which stood at 1.6%.

Scotland’s growth is evident when examining major cities, as Edinburgh came out on top, having experienced a significant increase of lets agreed at 19.7% year-on-year. This was followed by Birmingham, which saw growth of 16.1%. The only major city to observe a decline was Norwich at 0.7%.

“The persistent imbalance between demand and supply continues to be a major factor driving rental rates,” the report said. “Tax and regulatory changes, including the upcoming Renters’ Rights Bill, have led many landlords to exit the market, exacerbating stock availability issues. Those landlords who remain are passing on the burden of higher interest rates and energy costs to their tenants through rent increases.

“Our analysis of Q1 2025 reveals a private rental sector (PRS) that is in crisis. Supply of properties newly to let fell by 1% in the quarter compared to the prior year and is now 22% lower than the pre-pandemic year of 2019. It’s an unrelenting struggle for prospective tenants looking for a new property to let. The volume of all properties to let has hit yet another all-time low, with just 284k properties currently available across the whole of the UK. This is 18% less than Q1 2024 and 23% lower than pre-pandemic 2019.”

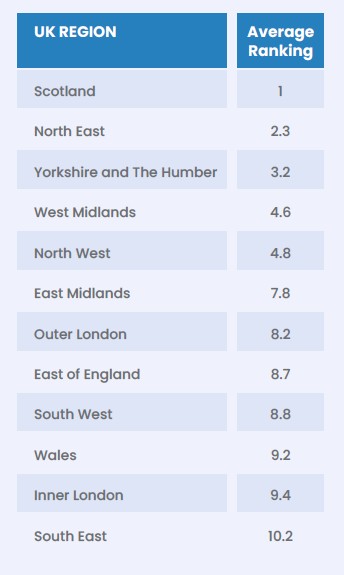

Reverting back to property sales, the South East was identified as the most challenging area to sell a property, with Scotland being the easiest. However, the result does not consider the regional price, with the average property listed for sale in Scotland in Q1 2025 is £232k, compared to £494k in the South East. “So, in terms of asset worth, the South East is a more appealing place to own a property, despite the difficulties of selling,” the report added.

The report also found that homemovers in 2025 are more affluent, more mature and earn comparatively higher incomes. When examining location changes, in general, accessible rural areas have become more important for the 2025 homemover, and this is at the expense of urban areas and remote rural areas. Looking regionally, there were more homemovers in the east of the UK. Those in the East Midlands are over 9% more likely to relocate in 2025, with the East of England exhibiting an increase of over 5% from last year. Conversely, home moves in 2025 have become significantly less likely in Scotland, with Northern Ireland, Wales, the North East and London also experiencing a decline in prevalence.

Colin Bradshaw, CEO at TwentyCi, said: “In Q1 2025, the UK property market saw the highest number of new listings in seven years, with strong demand driving a 9.3% increase in sales compared to Q1 2024. Detached houses were particularly sought after, while the average time to achieve a sale and to exchange both increased. Rental stock availability dropped by 16% year-on-year.

“In general, there are reasons for optimism but the key questions ahead are what will be the impact of global trade on the UK economy and moreover the impact on employment futures and how mortgage lenders react in terms of lending policy. Frankly, I have no idea, but with interest rates forecast to fall I suspect cautious optimism will serve us well.”